Europe Quartz Market Overview - Definition, scope, and significance?

The Europe Quartz market comprises the production, processing, and distribution of natural and engineered quartz materials used across a variety of industrial and consumer applications. Scope includes quartz surface and tile, high‑purity quartz, quartz glass, quartz crystal, and quartz sand, serving end‑users such as electronics and semiconductor, solar, construction, medical, optics, and telecommunications. Quartz is valued for its chemical stability, high thermal resistance, and exceptional mechanical properties, making it a cornerstone material for high‑tech components, durable building finishes, and renewable energy systems. The market’s significance lies in its role as an enabler of technological advancement and sustainable infrastructure within Europe.

Europe Quartz Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rapid expansion of the renewable‑energy sector, especially solar photovoltaics, growing demand for high‑performance electronic components, and robust construction activity driving quartz surface and tile consumption. Opportunities arise from emerging applications in medical diagnostics and advanced optics, where high‑purity quartz is essential. Restraints stem from fluctuating raw‑material availability and stringent environmental regulations governing quartz mining and processing. Challenges include price volatility of quartz sand and the need for significant capital investment in purification technologies, which can limit entry for smaller players.

Europe Quartz Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift toward engineered quartz surfaces that combine aesthetic appeal with durability, boosting market share for quartz surface and tile. In the high‑purity segment, demand is propelled by the proliferation of 5G networks and semiconductor miniaturization. An emerging trend is the integration of recycled quartz content in construction materials, aligning with circular‑economy objectives. Additionally, the adoption of quartz glass in aerospace and defense is gaining momentum due to its superior optical clarity and temperature resistance.

COVID-19 Impact on the Europe Quartz Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused temporary disruptions in supply chains, particularly in mining and logistics, leading to short‑term inventory shortages. However, the swift rebound of construction projects and accelerated digital transformation in electronics helped the market recover faster than many adjacent sectors. By late 2022, demand had returned to pre‑pandemic levels, and growth momentum continued, supported by stimulus measures aimed at green‑energy and infrastructure development across the European Union.

Europe Quartz Market Competitive Landscape - Major competitors and market consolidation?

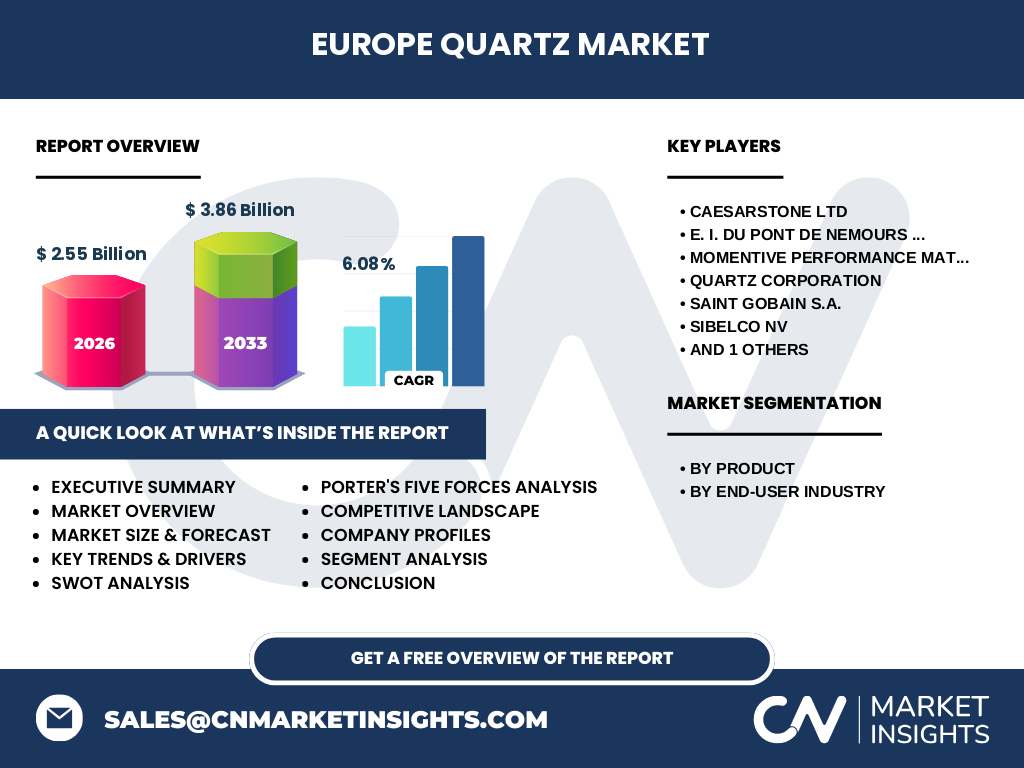

The competitive landscape is dominated by a mix of multinational corporations and specialized producers. Leading companies such as Caesarstone Ltd, E.I. Du Pont De Nemours and Company, Momentive Performance Materials Inc., Quartz Corporation, Saint‑Gobain S.A., Sibelco NV, and Thermo Fisher Scientific Inc. hold significant influence across the product spectrum. Recent years have witnessed strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach, indicating a moderate level of consolidation within the market.

Executive Summary - High-level overview and key findings about Europe Quartz Market?

The Europe Quartz market is projected to grow from a 2026 valuation of €2.55 billion to €3.86 billion by 2033, reflecting a compound annual growth rate of 6.08 %. Growth is driven by robust demand in electronics, solar energy, and construction, while high‑purity and quartz glass segments benefit from advances in telecommunications and aerospace. Environmental regulations and raw‑material price pressures present challenges, yet opportunities in recycling and new high‑tech applications provide a forward‑looking growth path. Major players are consolidating through acquisitions, positioning themselves for long‑term leadership.

Europe Quartz Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 6.08 %, the market is expected to maintain steady expansion throughout the 2025‑2032 horizon. The growth trajectory will be reinforced by continued investment in renewable‑energy infrastructure, escalating semiconductor demand, and increasing adoption of quartz‑based surfaces in residential and commercial construction. The forecast anticipates a balanced contribution from each product segment, with quartz surface and tile and high‑purity quartz leading in volume, while quartz glass and crystal capture higher value‑added opportunities.

Europe Quartz Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by product includes quartz surface and tile, high‑purity quartz, quartz glass, quartz crystal, and quartz sand. By end‑user industry, the market serves electronics and semiconductor, solar, buildings and construction, medical, and optics and telecommunications. While exact percentage shares are not disclosed, the broad diversification across these segments underlines the market’s resilience and capacity to offset downturns in any single vertical.

Global Europe Quartz Market Size and Share by Region - Geographic distribution?

Europe represents a key region within the global quartz landscape, contributing a substantial portion of worldwide demand due to its advanced manufacturing base and stringent quality standards. The market’s €2.55 billion size in 2026 underscores Europe’s pivotal role, with growth expectations aligned with the overall global expansion of quartz applications.

Regional Analysis of the Europe Quartz Market - Detailed regional market performance?

Within Europe, Western nations such as Germany, France, and the United Kingdom exhibit strong consumption of quartz surfaces for high‑end residential and commercial projects, while Southern countries like Spain and Italy are notable for solar‑panel quartz requirements. Eastern European economies are emerging as growth hubs for high‑purity quartz driven by expanding electronics manufacturing facilities. Regional policy incentives for green construction further stimulate demand across the continent.

Leading Company Profiles in the Europe Quartz Market - Industry players and strategies?

Caesarstone Ltd focuses on premium engineered quartz surfaces, leveraging design collaborations and sustainability certifications. E.I. Du Pont De Nemours and Company offers a wide range of high‑purity quartz for semiconductor and optics, emphasizing R&D and advanced purification. Momentive Performance Materials Inc. supplies specialty quartz glass and crystal, targeting aerospace and medical markets. Quartz Corporation concentrates on quartz sand and bulk raw material supply, ensuring stable feedstock for downstream users. Saint‑Gobain S.A. integrates quartz into building materials, promoting energy‑efficient construction solutions. Sibelco NV operates extensive mining assets, prioritizing environmentally responsible extraction. Thermo Fisher Scientific Inc. provides high‑purity quartz for scientific instruments, focusing on precision and reliability.

Porter's Five Forces Analysis of the Europe Quartz Market - Competitive forces assessment?

• Threat of new entrants: Moderate – high capital requirements and regulatory barriers limit newcomers.

• Bargaining power of suppliers: Moderate – limited number of high‑quality quartz mines grants suppliers some leverage.

• Bargaining power of buyers: High – large manufacturers can negotiate pricing, especially for bulk quartz sand.

• Threat of substitutes: Low – few materials match quartz’s combination of thermal stability and optical clarity.

• Industry rivalry: High – intense competition among established players drives innovation and price competition.

SWOT Analysis of the Europe Quartz Market - Strengths, weaknesses, opportunities, threats?

Strengths: Superior material properties, diversified end‑user base, strong engineering capabilities.

Weaknesses: Dependency on raw‑material availability, environmental compliance costs.

Opportunities: Growth in renewable energy, expansion of high‑purity quartz for 5G/6G, recycling initiatives.

Threats: Price volatility of quartz sand, tightening environmental regulations, geopolitical supply disruptions.

Europe Quartz Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material extraction (quartz mining), followed by beneficiation and purification processes. Next, specialized manufacturing transforms purified quartz into finished products such as engineered surfaces, glass, or crystals. Distribution channels include direct sales to OEMs, industrial distributors, and retail outlets for construction materials. End‑users—electronics manufacturers, solar panel producers, builders, and medical device companies—complete the chain, providing feedback that drives product innovation.

Key Investment Insights in the Europe Quartz Market - Strategic investment recommendations?

Investors should consider assets that enable vertical integration, such as securing mining rights or expanding purification capacity, to mitigate supply risk. Companies with a diversified product portfolio across surface, high‑purity, and glass segments are positioned to capture multiple growth vectors. Funding initiatives focused on recyclable quartz technologies aligns with sustainability trends and may attract favorable regulatory incentives. Partnerships with semiconductor and solar firms can accelerate market penetration.

Europe Quartz Market Conclusion - Summary and key takeaways?

The Europe Quartz market is on a solid growth path, underpinned by a 6.08 % CAGR and expanding demand across high‑tech and construction sectors. While raw‑material constraints and regulatory pressures present challenges, the market’s diversified applications and ongoing innovation create a resilient outlook. Major players are consolidating, and strategic investments in purification, recycling, and high‑value segments will likely yield the strongest returns.

Research Methodology - How this research was conducted?

The study combines primary interviews with industry executives, secondary data from company reports, trade publications, and government databases, and quantitative modeling based on the provided market size and forecast figures. Trend analysis and scenario planning were used to assess future dynamics, while competitive mapping identified key players and strategic moves.

Research Scope - Coverage and limitations?

The scope encompasses the full spectrum of quartz products and end‑user industries within Europe, covering market size, growth forecasts, segmentation, and competitive landscape. Limitations include the use of publicly available data only; proprietary financial details beyond the stated figures were not incorporated.

Key Companies and Recent Developments in the Europe Quartz Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Caesarstone Ltd’s launch of a new line of low‑VOC engineered quartz surfaces aimed at green‑building certifications. Du Pont announced a partnership with a leading European semiconductor fab to supply ultra‑high‑purity quartz for next‑generation chips. Momentive Performance Materials Inc. unveiled a breakthrough quartz glass composition with enhanced thermal shock resistance for aerospace applications. Quartz Corporation expanded its quartz sand mining capacity in Scandinavia to meet rising construction demand. Saint‑Gobain S.A. introduced a recyclable quartz‑based façade system targeting energy‑efficient retrofits. Sibelco NV secured an EU‑funded grant to develop environmentally friendly extraction techniques. Thermo Fisher Scientific Inc. released a high‑precision quartz crystal series for advanced analytical instruments.